Educational philanthropy is a prime example of human generosity and the will to help others. It is especially fruitful when geared into the education and productivity of the youth, and it perhaps seems luring as a break-down of the cynical premise of ‘rationality’ that is the life-blood of conventional economics.

But can good-natured, well-intentioned philanthropy not do the good it is meant to do? Could it even lead to elitism and inequality? Could it be… harmful? On the surface, one is inclined to say no (especially as a donor), but a deeper look is warranted:

If there’s only one seller of a product and new firms can’t enter the market, competition can’t drive prices down, as explained in this video after some nice black-and-white scene setting. Being a monopoly is nice work if you can get it.

Money quote: “Monopolistic competition, oligopolies / neither of them are efficient allocatively”

Counting Prof

Looking at the same topic from a different angle, this is so well-produced it looks like a proper music video. Read the rest of this entry »

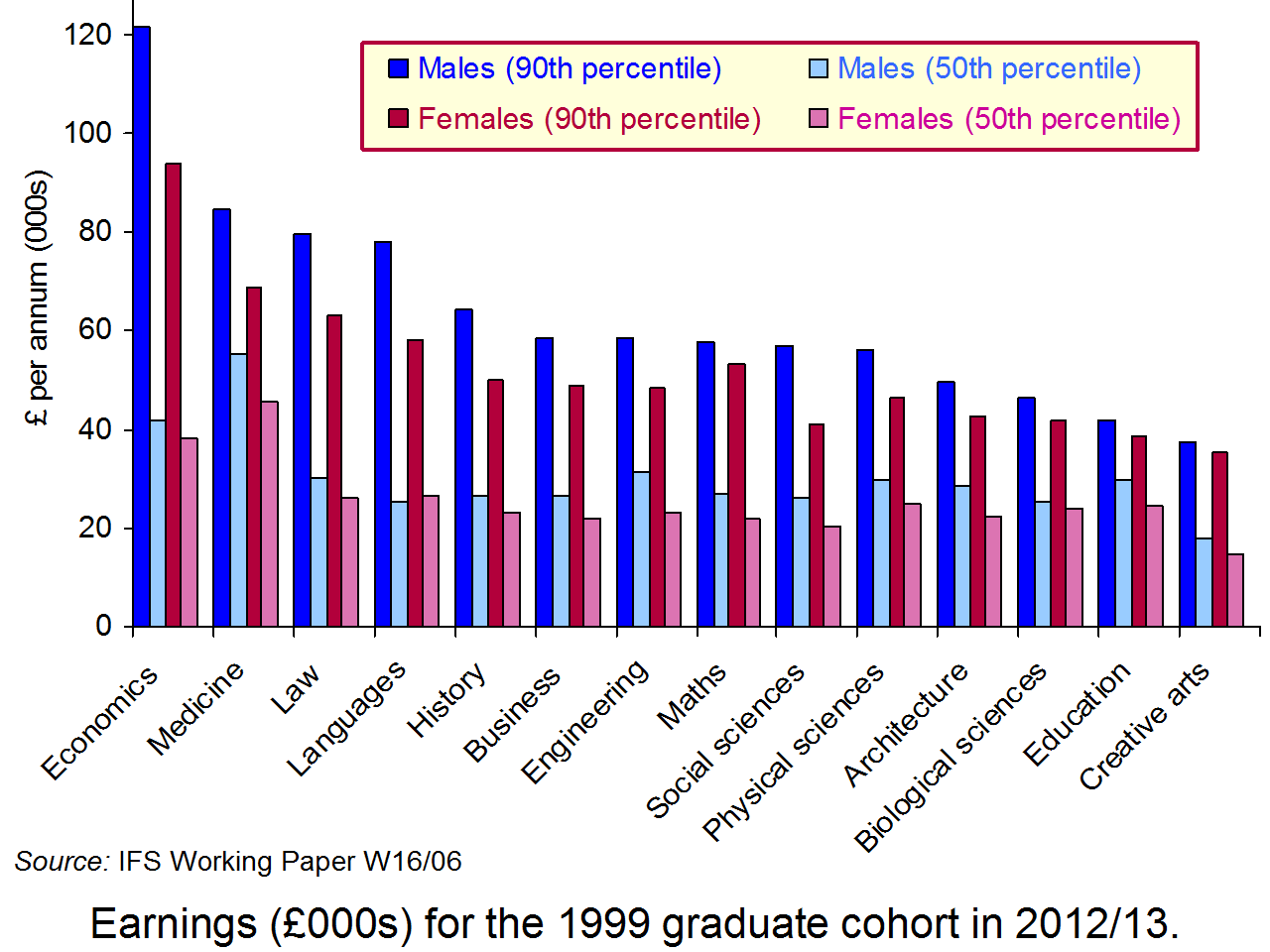

Anyone considering an Economics degree will find good news in research announced this week by the Institute for Fiscal Studies. It is a massive study, looking at what 260,000 university graduates in England are earning, ten years after graduating.

The IFS found “substantial” differences in the money people were earning, depending on the subject they took at university. Economists are most likely to be the top earners, by a clear margin. Read the rest of this entry »

For this story about the effect of economics in one person’s life, we thank guest author Elena Fernandez Prados for sharing an extract from her new book, Economics through Everyday Stories from around the World. ISBN 978-1523296415

Rachid Benchekroun is a software engineer from Casablanca, Morocco’s largest city. Rachid works for a technology company developing computer games and lives in an elegant villa around the corniche (waterfront promenade), one of Casablanca’s fanciest neighborhoods. But life has not always been easy for Rachid, and at the age of twenty-five, he feels that he has come a long way in life.

Rachid grew up in Casablanca’s suburbs, in a small one-bedroom apartment that he shared with his parents, his three siblings, and two of his cousins from the village. Abdel Karim, Rachid’s father, was a mechanic, while his mother, Fatima, was a homemaker. From an early age, Rachid learned the value of hard work. He attended school in the mornings and helped his father in the garage in the afternoons, oiling engines and pumping tires. At night, Rachid did his school homework diligently under a kerosene lamp. “Study hard, young boy,” his father often reminded him, “for it is the only way that the son of a mechanic from Chefchaouen can become someone in life.” Read the rest of this entry »

The Rockonomics competition, run by a group of US universities, gets students to write economics lyrics for popular songs and raps, and to make videos for them.

Some of these are pretty good ways to stick an economic idea in your head. Read on for our eight choices from the last few years of the competition. Read the rest of this entry »

Figures this released by the ONS on this week show that the UK has officially entered a recession; the second recession the UK has suffered in three years. David Cameron has said that these figures were very disappointing while Ed Miliband has called them catastrophic. But how catastrophic is a double dip recession for the UK? There are a number of reasons to doubt the media’s, and some politicians, doomsday predictions. Read the rest of this entry »